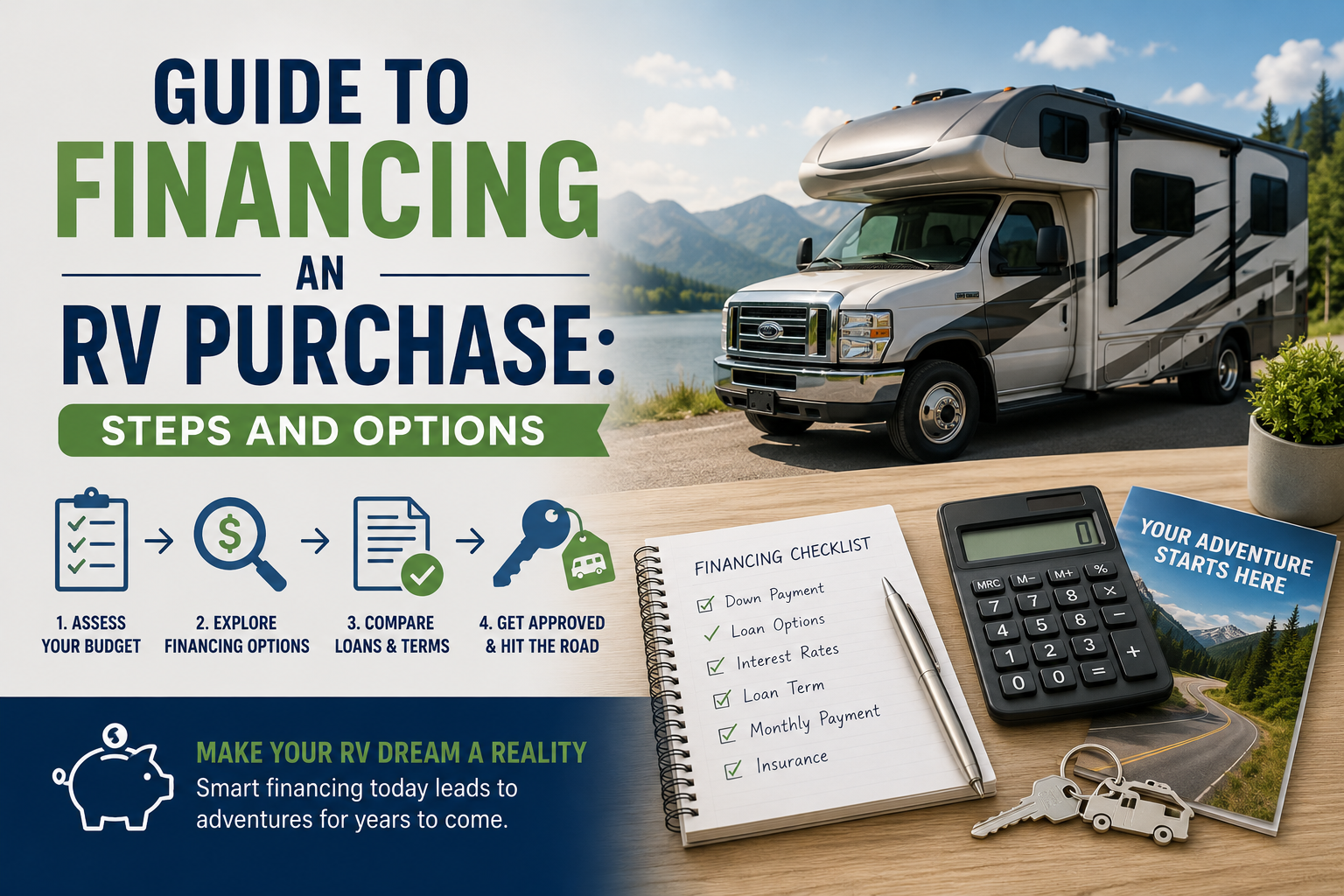

How to Finance an RV: Navigating Your Path to Adventure

Owning a Recreational Vehicle (RV) unlocks a world of freedom, allowing you to explore the open road with your home on-wheels. Whether you dream of weekend camping trips, cross-country tours, or a nomadic lifestyle, an RV can make it possible. However, for most prospective buyers, the significant upfront cost is the primary hurdle. An RV is a major purchase, often comparable to buying a house or a luxury vehicle. Therefore, understanding how to finance an RV is a critical step in turning your dream into reality.

This guide will walk you through the various financing options, key considerations before you apply, and strategic tips to secure the best possible loan for your new adventure vehicle.

Understanding RV Financing: It’s Not Just a Car Loan

While an RV loan shares similarities with an auto loan, there are crucial distinctions that affect the process, terms, and requirements.

RV Loans Are Typically Secured Loans: The RV itself serves as collateral for the loan. If you default, the lender can repossess it. This security often allows for longer loan terms and potentially lower rates compared to unsecured personal loans.

Loan Terms Are Longer: Given the higher purchase price, which can range from $30,000 for a modest travel trailer to over $500,000 for a luxury motorhome, loan terms extend well beyond the typical 5-6 years for a car. RV loans commonly range from 10 to 15 years, and sometimes even up to 20 years for high end models.

Classification Matters: Lenders categorize RVs differently, which impacts financing.

- Motorized RVs: These are self-propelled, like Class A, B, or C Motorhomes. They are often financed similarly to vehicles but with longer terms.

- Towable RVs: These include Travel Trailers, Fifth Wheels, and Pop-up Campers. They are considered collateral, but your ability to tow them (having a suitable tow vehicle) can be a factor for some lenders.

Example Scenario:

John is looking at a new Class C motorhome priced at $85,000. He secures a loan with a 12-year term at a 6.5% interest rate. His monthly payment would be approximately $850. A similar-priced luxury SUV with a 5-year loan at 4.5% would have a monthly payment of nearly $1,600. The longer term makes the RV purchase more manageable on a monthly budget, though it means paying more interest over the life of the loan.

Key Considerations Before You Seek Financing

Before you walk into a dealership or contact a lender, take these essential steps.

1. Establish a Realistic Budget

This goes beyond the sticker price. Create a comprehensive budget that includes:

- Down Payment: Most RV loans require a minimum down payment, typically 10-20%. A larger down payment reduces your loan amount, monthly payments, and total interest cost.

- Monthly Payment: Use online calculators to estimate payments based on price, term, and estimated interest rate. Ensure this fits comfortably within your monthly finances.

- Total Cost of Ownership: Factor in insurance, registration, maintenance, storage fees (if not parked at home), and campground costs. Fuel for motorized RVs can be a significant ongoing expense.

2. Check Your Credit Score

Your credit score is the most critical factor in determining your loan eligibility and interest rate.

- Excellent Credit (720+): You’ll qualify for the best advertised rates from most lenders.

- Good Credit (680-719): You’ll still get favorable rates, but may not get the absolute lowest.

- Fair Credit (620-679): You will likely qualify, but at higher interest rates.

- Poor Credit (Below 620): Financing becomes challenging. You may need a very large down payment, accept a high-rate loan, or seek a specialized subprime lender.

It’s wise to check your credit report for errors and understand your score before applying.

3. Decide on New vs. Used

This choice significantly impacts financing.

- New RVs: Easier to finance with standard lenders, often come with promotional manufacturer rates (especially at dealerships), and have full warranties. However, they depreciate quickly.

- Used RVs: Generally cheaper upfront. Financing can be more restrictive, many lenders have age and mileage limits (e.g., no older than 10-15 years). Interest rates for used RVs are often higher. However, the depreciation curve has flattened, offering better value.

Primary RV Financing Options

You have several avenues to secure an RV loan. Here are the most common.

1. Dealership Financing

This is the most convenient option, as you can arrange the purchase and financing in one place.

Pros:

- Convenience: Streamlined, one-stop process.

- Promotional Offers: Manufacturers often provide low-interest promotional rates (sometimes as low as 3-4%) on new models to incentivize sales.

- Relationship: Dealers work with multiple lenders and can sometimes help borrowers with less-than-perfect credit.

Cons:

- Potentially Higher Rates: Outside of promotions, dealership rates may not be the most competitive.

- Focus on Sale: The finance manager’s primary goal is to complete the sale. It’s essential to review the terms carefully.

Tip: Always get a pre-approved loan from another source before going to the dealership. This gives you a rate to compare against and makes you a “cash buyer” in negotiations, potentially strengthening your position on the purchase price.

2. Banks and Credit Unions

Traditional financial institutions are a major source of RV loans.

Credit Unions: Often offer the most competitive rates to their members. They are known for personalized service and may be more flexible. If you belong to a credit union, start your search here.

National and Local Banks: Many large banks have dedicated RV and boat lending departments. They offer standardized processes and may have robust online tools.

Pros:

- Competitive Rates: Especially from credit unions.

- Existing Relationship: If you have a long-standing relationship, the process may be smoother.

- Transparency: Terms are usually clear and straightforward.

Cons:

- Strict Criteria: Banks may have stricter credit and income requirements.

- Less Flexible: Might not finance older or unique RVs.

3. Specialty RV Lenders

These are financial institutions that focus exclusively on RV, marine, and aircraft loans. They understand the RV market intimately.

Pros:

- Expertise: They know how to appraise RVs and understand their value.

- Flexibility: Often more willing to finance used, older, or high-value RVs.

- Long Terms: Typically offer the longest loan terms available (up to 20 years).

Cons:

- Rates: While competitive, they might not always beat a credit union’s best offer.

- Not Local: Usually operate online or via phone, which some borrowers may find less personal.

4. Personal Loans

An unsecured personal loan from a bank, online lender, or peer-to-peer platform is an option, especially for smaller RV purchases or used models that don’t qualify for traditional RV loans.

Pros:

- Fast: Can be obtained very quickly.

- No Collateral: The RV isn’t tied as collateral, which can be advantageous if you have other plans for it.

Cons:

- Higher Rates: Interest rates are significantly higher than secured RV loans.

- Short Terms: Terms are usually limited to 5-7 years, leading to high monthly payments.

- Lower Amounts: Loan amounts may not cover the cost of a larger RV.

This option is generally best only for small, inexpensive towable trailers or as a last resort.

The Step-by-Step Financing Process

Once you’ve chosen your preferred financing path, follow these steps.

- Get Pre-Approved: Contact your chosen lender(s) and get pre-approved for a loan. This involves a soft credit check and gives you a maximum loan amount, estimated rate, and term. This knowledge is power when you start shopping.

- Shop for Your RV: With your budget and pre-approval in hand, you can confidently shop for the RV that fits your needs and finances.

- Finalize the Purchase Agreement: Negotiate the final price with the seller or dealer. Ensure all costs (tax, title, fees) are outlined.

- Submit Final Loan Application: Provide the lender with the final details: the exact RV model, year, VIN, and purchase agreement. They will perform a hard credit check and official underwriting.

- Loan Closing: The lender will send closing documents (often electronically). You’ll sign the loan agreement, which details the interest rate, term, monthly payment, and all terms.

- Funds Disbursement: The lender will pay the seller (dealership or private party). You’ll make your down payment directly to the lender or seller as arranged.

- Take Ownership: You receive the title (often held by the lender until the loan is paid) and the keys! Don’t forget to insure the RV immediately.

Smart Tips for Securing the Best RV Loan

- Shop Around: Never accept the first offer. Get quotes from at least a dealership, a credit union, and a specialty lender.

- Improve Your Credit: If time allows, take steps to improve your credit score: pay down debts, correct errors on your report, and avoid new credit applications.

- Consider a Co-Signer: If your credit is weak, a co-signer with strong credit can help you qualify for a much better rate.

- Calculate the Total Interest Cost: A longer term lowers the monthly payment but increases the total interest paid over the life of the loan. Use an amortization calculator to see the true cost. Sometimes, a shorter term with a higher monthly payment is more economical in the long run.

- Read the Fine Print: Understand all loan fees (origination fees, prepayment penalties), insurance requirements, and what happens if you want to sell the RV before the loan is paid off.

Conclusion

Financing an RV is a deliberate process that, when done correctly, can make your dream vehicle affordable without straining your finances. The key is to approach it with preparation: know your budget, understand your credit, research the different types of lenders, and always compare multiple offers. Remember, the goal is not just to acquire an RV, but to do so in a way that preserves your financial health, allowing you to enjoy the adventures it brings for years to come. With the right loan in place, the road ahead is open and waiting.